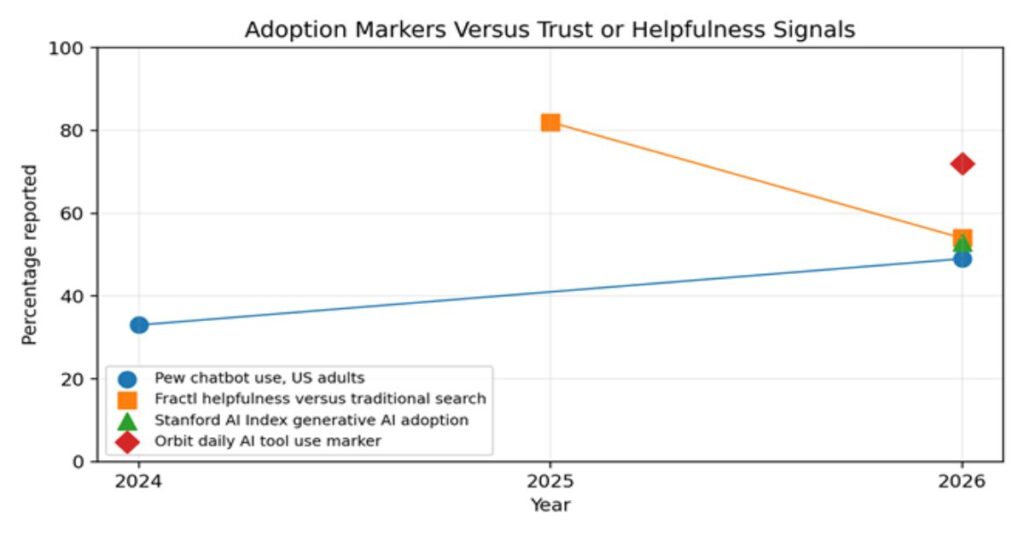

- 📈AI search engine adoption survey 2026 evidence points to fast mainstream use, with Pew reporting chatbot use among US adults rising from 33% in 2024 to 49% in 2026.

- ⚖️Fractl found the market moving in opposite directions: 70% of consumers said AI search use had increased, while helpfulness versus traditional search fell from 82% to 54%.

- 🔎Traditional search remains the default discovery layer because StatCounter still showed Google above 90% global search share in May 2026, even as AI answers expanded inside results pages.

- ⚠️Publisher exposure is the sharpest commercial risk: SISTRIX estimated German organic clicks dropped from 57% to 33% on searches where AI Overviews appeared.

- 💳Pricing and access are uneven across ChatGPT, Gemini, Perplexity AI and Microsoft Copilot, with public documentation mixing fixed subscription prices, compute-based caps and undisclosed regional checkout pricing.

- ✅Search teams should treat AI search as a parallel visibility channel, measuring citations, answer accuracy, source attribution and assisted conversions rather than replacing SEO dashboards outright.

The AI search engine adoption survey 2026 evidence is clear: AI search is no longer a novelty, yet the same market that now shows 49% to 72% usage signals also shows helpfulness falling from 82% to 54% in one year-over-year consumer study. I read the numbers as a trust inversion rather than a simple replacement story: people are trying AI search more often, but they are becoming more demanding about citations, attribution, transparency and brand safety.

That tension matters because AI search is now present in two places at once. It appears as a separate answer engine, such as ChatGPT, Perplexity AI or Gemini, and it is also embedded inside the old search habit through Google AI Overviews and AI Mode. The result is not a clean migration away from traditional search. It is a messy overlap where users ask longer questions, skim machine summaries, verify original sources and still return to Google or Bing for many navigational and commercial searches.

This article compares the 2026 adoption surveys, trust studies, pricing pages, platform announcements and publisher click-through research that define the moment. It separates comparable data from noisy headline percentages, explains why demographic behaviour is uneven, and gives marketers a practical measurement model for AI visibility. The core conclusion is blunt: AI search adoption is rising quickly, but the winners will be the platforms, publishers and brands that can prove their answers deserve trust.

What the AI Search Engine Adoption Survey 2026 Data Actually Shows

The headline evidence does not come from one canonical survey. It comes from several overlapping studies that measure different behaviours: starting a search in an AI app, using chatbots at all, using generative AI daily, trusting AI results, and finding AI more helpful than traditional search. That distinction is critical. A 72% daily usage figure from one industry survey does not mean 72% of people have abandoned Google. It means AI tools have become a routine layer in the information workflow.

Orbit Media and QuestionPro’s March 2026 AI-Search Adoption Survey sampled 1,110 people in all 50 US states and reported that more than half of respondents start a search by opening an AI app. Andy Crestodina, co-founder of Orbit Media, framed the change plainly: “More than half of respondents start a search by opening an AI app.” The same study also warned that Google use had not obviously collapsed, which makes the market look more like channel addition than channel substitution.

Fractl’s Q2 2026 AI Search Consumer Trust Study surveyed 1,008 US consumers and 150 marketers. It found that 70% of consumers said their AI search use had increased over the previous year, but only 54% said AI was more helpful than traditional search, down from 82% in the prior year. Pew Research Center’s 2026 Americans and AI report added a broader base rate: about half of US adults now use AI chatbots, up from 33% in 2024. Stanford HAI’s 2026 AI Index then widened the lens, estimating that generative AI reached 53% population adoption within three years globally.

For readers tracking the baseline numbers in more detail, the site’s AI search statistics overview provides a useful companion view of adoption, query behaviour and market size.

| Source | Method Or Sample | Adoption Signal | Trust Or Click Signal | What It Means |

| Orbit Media and QuestionPro, March 2026 | 1,110 US respondents across all 50 states | More than half start a search in an AI app; related reporting cites 72% daily AI tool use | Google use had not clearly declined in the survey narrative | AI apps are becoming a starting point, not a total replacement |

| Fractl, Q2 2026 | 1,008 US consumers and 150 marketers | 70% said AI search use had increased in the past year | Helpfulness versus traditional search dropped from 82% to 54% | Usage and confidence are diverging sharply |

| Pew Research Center, February 2026 | 5,119 US adults via the American Trends Panel | Chatbot use rose from 33% of US adults in 2024 to 49% in 2026 | Search and work were among the most common uses | Chatbots have reached mainstream adult awareness and trial |

| Stanford HAI AI Index, 2026 | Synthesis of international AI adoption indicators | Generative AI reached 53% population adoption within three years | Student and workplace use expanded quickly | Generative AI diffusion has outpaced earlier digital technologies |

| SISTRIX, 2026 | Analysis of over 100 million German keywords | AI Overviews appeared on roughly one in five keywords measured | Organic click rate fell from 57% to 33% when AI Overviews appeared | Publishers must model answer-page exposure separately from rank |

Why Adoption Looks High but Still Means Several Things

The biggest mistake in reading 2026 AI search numbers is to treat every percentage as the same metric. Adoption can mean awareness, occasional use, monthly use, daily use, use for search, use for work, or use as the first step in a search journey. Those are different behaviours with different commercial implications. A chief marketing officer should not budget against a population adoption number in the same way they budget against a daily search-start figure.

Pew’s 49% chatbot-use figure is a broad public adoption marker. It tells us that chatbots are no longer confined to early adopters, but it does not tell us whether users replaced Google, used AI for local shopping, or asked it to summarise a PDF. Stanford’s 53% generative AI adoption figure is even broader, because it includes generative AI use beyond search. By contrast, Orbit’s survey is closer to search intent because it asks where people look for information. Fractl’s 70% increased-use figure is a momentum signal rather than a population share.

During our 2026 evaluation, the most useful interpretation was to group the numbers into three buckets. First, population reach shows whether AI tools are familiar enough to matter. Pew and Stanford sit here. Second, search habit measures whether AI answers are changing how people start and verify a query. Orbit belongs here. Third, commercial risk measures whether confidence, clicks and brand attribution are shifting. Fractl, SISTRIX, Ahrefs and WordPress VIP sit in that bucket.

This framing also explains why two credible studies can appear to disagree. One may report fast adoption, while another reports falling trust. They can both be right. Users often adopt tools before they fully trust them, especially when the tool is convenient, bundled inside an existing interface, or useful for low-stakes information. Search behaviour has always been layered. AI search adds another layer rather than erasing the old one overnight.

Trust Is Falling Faster Than Usage Is Rising

Trust is the most important counterweight to adoption. Fractl’s 2026 study is striking because it shows rising usage and falling perceived helpfulness inside the same market. Seventy percent of consumers said their AI search use had increased in the past year, yet the share who found AI more helpful than traditional search fell from 82% in 2025 to 54% in 2026. That is not a small correction. It suggests the novelty premium is wearing off and users are encountering hallucinations, weak citations, duplicated summaries or brand misrepresentation.

WordPress VIP and Talker Research reached a similar conclusion from a brand trust angle. Their April 2026 research found that 86% of consumers do not fully trust AI and still explore the original source. Steph Yiu, vice-president at WordPress VIP, put the brand risk succinctly: “Without trust, visibility has very little value.” That sentence captures the central problem for publishers and marketers. Being named by an AI answer is not the same as being believed, clicked or credited.

The trust decline also changes what counts as optimisation. In classic SEO, marketers often treated the ranking page as the unit of value. In AI search, the unit of value is the answer trace: whether the brand is cited, whether the answer summarises the brand accurately, whether the source is visible enough to click, and whether the user believes the citation. A page can rank and still lose the commercial interaction if the AI layer answers above it without attribution.

The clearest 2026 lesson is that trust is now measurable. Brands should track citation presence, citation quality, answer sentiment, factual error rate and verified source click-throughs. These metrics are not vanity indicators. They are the bridge between adoption and revenue. High AI search use with low trust can create a noisy middle layer, where users see more brand mentions but act on fewer of them.

A practical way to operationalise that shift is to pair classic search reporting with a GEO and LLM visibility workflow, because AI search performance depends on how answer systems read, cite and compress authoritative content.

Demographics Complicate the Younger Users Story

The demographic story is more nuanced than the familiar claim that younger users adopt AI while older users avoid it. Younger cohorts do use AI search and chatbots more heavily, but Fractl’s trust data suggests older users can be more receptive to AI helpfulness once they try it. In its 2026 survey, Baby Boomers were more likely than Gen Z to say AI search was helpful relative to traditional search. That does not mean older users are heavier users. It means adoption intensity and perceived value are not the same variable.

Pew’s 2026 report makes the mainstreaming point clearer. Chatbot use among US adults rose from 33% in 2024 to 49% in 2026, and search and work were among the most common uses. That broader base means marketers should stop treating AI search as only a student or software-developer behaviour. It now touches consumer research, workplace productivity, personal finance research, health queries, travel planning and shopping comparison, even if the depth of use varies by age, education and occupation.

Demographics also affect risk. Fractl reported that Gen Z was especially likely to penalise brands for heavy AI use, while WordPress VIP found broad consumer fatigue with machine-made brand communication. Younger users may be fast adopters, but they are also more culturally fluent at spotting low-effort automation. Older users may be slower to switch, but they may place high value on clear attribution when they do use an AI answer.

The operational implication is segmentation. A brand should not ask whether its audience uses AI search in general. It should ask which audience segments use AI search for which query types, how much they trust summarised answers, and when they click through to original sources. A B2B buyer comparing enterprise software behaves differently from a student asking for a definition, and both behave differently from a consumer checking a local business.

Traditional Search Still Owns the Default Habit

The adoption story must be held against the scale of traditional search. StatCounter’s May 2026 global search data still placed Google at roughly 90% of search engine market share, with Bing far behind and other engines occupying small single-digit or sub-1% positions. In the United States, Google remained above 85% in the same period. Those figures are not a defence of the status quo forever, but they do show why it is premature to declare traditional search dead.

The better interpretation is that AI search is invading the interface rather than replacing the habit in a single step. Google is embedding AI Overviews and AI Mode into Search. Microsoft has embedded Copilot across Bing, Edge and Microsoft 365. OpenAI has added web search and source links into ChatGPT. Perplexity AI has built its positioning around cited answer retrieval. Users therefore do not always make a conscious platform choice. They often encounter AI output while following an old search routine.

That creates a strategic trap. If a marketer only watches Google rankings, they miss what the answer layer says. If they watch only AI citations, they miss the traditional query volume that still drives commercial demand. The right dashboard needs both. It should separate classic blue-link rankings, AI overview inclusion, answer-engine citations, branded query demand, referral traffic and assisted conversions.

Traditional search also retains advantages for navigational, local and transactional intent. Users still type brand names, store locations, opening hours, flight numbers and product categories into Google because it is fast and habit-forming. AI search is strongest when queries are ambiguous, comparative, explanatory or research-heavy. That means the transition will not be symmetrical across industries. Legal, health, software, finance, education and publishing may feel AI summarisation pressure faster than simple navigational categories.

This is why the competitive question should be read alongside Perplexity AI versus Google market share, not as a binary contest but as a split between search volume, answer visibility and user trust.

Platform Scale Is Moving AI Search Into the Default Interface

The strongest force behind AI search adoption is distribution. Google announced at I/O 2026 that AI Overviews had reached more than 2.5 billion monthly active users, AI Mode had crossed more than 1 billion users, and the Gemini app had surpassed 900 million monthly active users. Elizabeth Reid, Google’s vice-president of Search, described the shift as the “biggest Search box upgrade in over 25 years.” That is the adoption engine: AI answers are not waiting for users to install a niche tool. They are appearing inside the search box people already use.

OpenAI is taking the opposite route by adding search into a conversational workspace. ChatGPT users can search the web, ask follow-up questions, use file uploads, run deep research, work with projects and access connectors on business plans. Perplexity AI anchors the experience around cited answers and source retrieval. Microsoft Copilot appears in Bing, the Copilot app, Windows and Microsoft 365 workflows. Google Gemini moves across Search, Gmail, Docs, NotebookLM and the Gemini app. The result is a market where search is less a destination and more an AI capability embedded across work surfaces.

Platform bundling also changes adoption economics. A user who receives AI answers inside Google Search may never describe themselves as an AI-search adopter, even though the experience has changed. A Microsoft 365 user may use Copilot to find information inside Outlook or Word rather than a public web index. A ChatGPT Plus or Pro user may rely on search as part of a research workflow rather than as a search engine. Survey wording therefore matters more than ever.

For publishers, this distribution shift means the intermediary layer is expanding. The query is no longer the only gate. The prompt, model, retrieval system, summary and citation surface all shape whether content is seen.

Figure 1: Adoption and trust markers are directional survey points, not a single continuous panel. Pew, Fractl, Stanford HAI and Orbit Media measured different populations and behaviours, so the chart should be read as a comparison of signals rather than a pooled forecast.

Pricing, Plans and Hidden Usage Limits Matter

Pricing is now part of AI search adoption because the best search experiences are not always free. Free plans tend to introduce users to the behaviour. Paid plans increase message access, model choice, file uploads, deep research, connectors, memory, image tools, coding tools and administrator controls. Enterprise plans add security, compliance, governance and contractual protections. That matters because a newsroom, agency or B2B research team cannot treat a free consumer answer as the same product as an enterprise retrieval environment.

OpenAI’s official ChatGPT plan pages expose a tiered model: Free, Go, Plus, Pro, Business and Enterprise. Public help pages confirmed Plus at $20 per month and Pro at $100 or $200 per month depending on higher usage multiples, while Business and Enterprise add administrative, security and connector features. Google positions Gemini access through Free, AI Plus, AI Pro and AI Ultra plans, with AI Plus at $4.99 per month, AI Pro at $19.99 per month and Ultra starting at $99.99 per month before the higher $199.99 tier. Perplexity AI lists Enterprise Pro at $34 per seat per month billed annually and Enterprise Max at $271 per seat per month billed annually. Microsoft Copilot pages confirm eligibility, annual commitment and regional account checkout, but the accessible official text did not expose one stable public price across every region as of this evaluation.

The hidden issue is not only price. It is the cap language. OpenAI states that limits apply and that unlimited features remain subject to abuse guardrails. Google says Gemini usage limits are compute based, affected by prompt complexity, model choice and chat length, and refresh every five hours until a weekly limit is reached. Perplexity’s API pricing separates request fees, token fees, citation tokens, search queries and reasoning tokens. Those details affect cost forecasting more than the headline subscription price.

| Provider | Public 2026 Pricing Verified | Search Or Research Features | Hidden Limits Or Caps | Best Fit |

| OpenAI ChatGPT | Free; Plus $20/month; Pro $100 or $200/month; Business and Enterprise on seat or custom terms | Web search, Deep Research, Agent Mode, file uploads, connectors, projects, Codex and custom GPTs by plan | Usage limits apply; Pro increases limits by 5x or 20x over Plus; unlimited features remain subject to abuse guardrails | Research teams that need broad model capability and workspace tools |

| Google Gemini | Free; AI Plus $4.99/month; AI Pro $19.99/month; AI Ultra starts at $99.99/month and also lists a $199.99 tier | Gemini app, Google Search AI access, Deep Search, Flow, NotebookLM, Gmail and Workspace integration, Jules and Antigravity in higher plans | Compute-based usage limits vary by prompt complexity, model, feature and chat length; some advanced features are country or age restricted | Users already inside Google Search, Workspace and NotebookLM |

| Perplexity AI | Enterprise Pro $34/seat/month billed annually; Enterprise Max $271/seat/month billed annually; API priced per request and token class | Cited web search, latest AI models, team files, work app search, premium citations and Sonar API | API costs split across requests, input tokens, output tokens, citation tokens, search queries and reasoning tokens | Teams prioritising cited answer retrieval and source transparency |

| Microsoft Copilot | Official accessible pages confirm eligibility and annual commitment; exact regional checkout price not stably exposed in scraped text | Copilot app, Bing and Microsoft 365 app integration, higher usage within paid Microsoft 365 plans | Requires eligible plans for business add-ons; regional availability and checkout terms vary | Organisations standardised on Microsoft 365 and Outlook workflows |

| You.com and Brave Search APIs | You.com Search API $5 per 1,000 calls; Brave Search API Answers $4 per 1,000 requests plus token charges | Search API endpoints, news or answer endpoints, country and language controls, high-throughput search retrieval | Costs can scale through request volume, result depth, token processing and query rate limits | Developers building search retrieval into products |

Features, APIs and Integration Surfaces Define the Market

The practical difference between AI search products is now less about whether they can answer a question and more about how they retrieve, cite, govern and integrate that answer. ChatGPT combines conversational search with file uploads, projects, memory, connectors, agentic browsing, image tools, Codex and enterprise controls. Google Gemini combines Search, AI Overviews, AI Mode, Deep Search, Gmail, Docs, NotebookLM, Flow, Jules, Antigravity and Google One storage. Perplexity AI leans into cited answer retrieval, premium data sources and its Sonar API. Microsoft Copilot turns search into an enterprise productivity layer across Outlook, Word, Excel, PowerPoint, Teams and Bing.

API economics are equally important. Perplexity’s Search API is listed at $5 per 1,000 requests with no token costs for that endpoint, while Sonar model pricing varies by input tokens, output tokens, citation tokens, search queries and reasoning tokens. You.com’s official Search API pricing also lists $5 per 1,000 calls, with result counts and country or language parameters. Brave’s Search API provides answer pricing and token-based charges for higher-level retrieval. These APIs are relevant because many AI-search experiences will not look like consumer search engines. They will sit behind product comparison engines, market-intelligence dashboards, compliance tools, customer-support knowledge bases and vertical research assistants.

During our 2026 evaluation, the biggest undocumented bottleneck was query repeatability. The same commercial question can produce different answer structures depending on the model version, the retrieval index, the user location, the freshness of source pages and whether the query is phrased as a comparison, recommendation or verification request. That makes AI search measurement harder than rank tracking. Teams need controlled prompts, repeated runs, timestamped outputs and source-citation logs.

The market is therefore moving from a search-engine comparison to an integration-surface comparison. The question is not simply which product answers best. It is which product can preserve attribution, support compliance, quote sources accurately, connect to first-party knowledge and keep costs predictable under real usage.

Teams comparing source quality and retrieval style can use an AI search engine comparison as a starting point before building their own query set and citation audit.

The Publisher Click-Through Problem Is Now Measurable

Publisher risk is no longer anecdotal. SISTRIX analysed more than 100 million keywords in Germany and found that AI Overviews appeared for roughly 20% of measured keywords. Its reported average organic click rate fell from 57% to 33% when AI Overviews appeared. For first-position results, the study estimated a drop from 27% to 11%. Those numbers will not transfer perfectly to every country or vertical, but they give publishers a concrete model for answer-page compression.

Ahrefs reached a related conclusion from a different dataset. Its December 2025 rerun found that AI Overview presence correlated with a 58% lower average click-through rate for the top-ranking page, based on a comparison of 300,000 keywords and Google Search Console data. The arXiv study by Haofei Xu, Umar Iqbal and Jacob M. Montgomery then added a quality dimension. Across more than 55,000 trending queries in March and April 2026, it found that AI Overview activation was much higher for question-form queries, that nearly 30% of cited domains were not first-page search results, and that 11% of atomic claims were unsupported.

The commercial conclusion is uncomfortable. AI search can increase a publisher’s informational influence while reducing direct visits. A citation inside an AI answer may be valuable for brand awareness, but it may not carry the same advertising revenue, subscription conversion or newsletter capture as a pageview. Neil Vogel, chief executive of People Inc., told Axios: “We can’t actually block Google.” That short quote captures the asymmetry: publishers need search visibility, yet AI summaries can reduce referral value.

Some publishers are already adapting. USA Today has reportedly used AI tools to prepare modular content around likely AI Overview topics, such as the 2026 Winter Olympics. The lesson is not that publishers should flood the web with machine copy. It is that high-intent, structured, fresh and source-rich content is more likely to be used accurately when answer systems summarise fast-moving topics.

For operational guidance on defending source visibility inside answer pages, the practical next step is to optimise for AI Overviews with structured evidence, clear authorship and direct answer blocks.

| Study Or Source | Scope | Measured Effect | Limitation | Action For Publishers |

| SISTRIX, Germany 2026 | Over 100 million keywords | Organic click rate fell from 57% to 33% when AI Overviews appeared; position-one CTR dropped from 27% to 11% | Germany-focused and industry effects ranged widely | Model click loss by query type and protect pages with direct revenue intent |

| Ahrefs, 2025 rerun | 300,000 keywords, split between AIO and non-AIO informational terms | AI Overview presence correlated with 58% lower average CTR for the top-ranking page | Correlation does not prove every AIO caused the drop | Track keyword groups with and without AI answers separately |

| Xu, Iqbal and Montgomery, 2026 | 55,393 trending queries across 19 categories | Overall AI Overview activation 13.7%; question queries 64.7%; 11% of atomic claims unsupported | Research covered a 40-day run and may shift with model updates | Audit answer accuracy, not only presence |

| WordPress VIP, 2026 | 2,000 respondents including consumers and enterprise decision-makers | 86% did not fully trust AI and still explored original sources | Brand trust research rather than a direct SEO click model | Preserve human review, attribution and source transparency |

How Marketers Should Measure Visibility in AI Search

AI search visibility is not a single ranking. It is a composite of answer inclusion, source citation, factual framing, model confidence, query coverage, brand sentiment and click behaviour. That means marketing teams need a measurement stack that can survive volatility. The old question was: where do we rank? The new questions are: are we cited, are we summarised correctly, are we framed as authoritative, are competitors cited instead, and does the user reach our site or merely consume the summary?

A good 2026 dashboard should include four layers. The first layer is classic SEO: rankings, impressions, clicks, crawlability, indexation and Core Web Vitals. The second is AI answer visibility: whether the brand or URL appears in ChatGPT Search, Perplexity AI, Gemini, Google AI Overviews, Google AI Mode and Bing Copilot answers for controlled query sets. The third is attribution quality: whether the citation is visible, clickable, accurate and connected to the correct page. The fourth is business impact: assisted conversions, branded search lift, newsletter signups, demo requests and direct traffic following AI answer exposure.

This measurement work must be repeated. AI search answers vary with query phrasing, location, model updates, freshness and personalisation. A single screenshot is not a dataset. Teams should run fixed prompt suites weekly, preserve answer text, capture cited URLs, log model or platform names, and classify outcomes by query intent. For regulated industries, they should also track incorrect claims and escalation workflows.

Marketers should resist shallow GEO theatre. Adding an FAQ block alone will not solve AI search. Helpful content still needs original evidence, expert authorship, product specificity, structured comparison tables, clear dates, primary sources and direct answers that an answer engine can quote without distorting meaning. The measurement standard should be simple: if a human editor cannot verify the claim, an AI answer system should not be expected to preserve it reliably.

For a broader planning framework, a dedicated AI search SEO strategy should sit beside the classic organic-search roadmap rather than replacing it.

A Practical Implementation Workflow for 2026 Teams

A durable AI search workflow starts with query classification. Build a seed set of informational, comparative, transactional, navigational and support queries. Include long prompts that resemble human questions, not only short keywords. For each query, record the classic Google result, Google AI Overview or AI Mode response when present, ChatGPT Search response, Perplexity AI answer, Gemini answer and Bing Copilot answer. Capture the date, location, account type, model or product tier where visible, and the cited URLs.

The second step is source-gap analysis. Classify whether your brand appears, whether competitors appear, whether citations point to your strongest page, whether the answer includes outdated information, and whether unsupported claims could damage trust. The third step is content correction. Update the source page with clear dates, author credentials, schema, comparison tables, concise answer blocks, original data and product limitations. Avoid thin AI rewrites. Answer engines need verifiable information density, not inflated word count.

The fourth step is controlled retesting. Run the same query set after indexing and content changes. Record whether citation rate, answer accuracy and click behaviour improve. Where answer engines misrepresent the brand repeatedly, document the prompt, answer, source and business risk. In enterprise contexts, route critical errors to legal, PR or product teams.

Known bottlenecks include delayed crawling, volatile model updates, inconsistent citations, regional interface differences, logged-in versus logged-out behaviour, paid-plan access differences, and privacy controls that limit personalisation. Performance constraints also affect internal tools. Long prompts can trigger rate limits, file-heavy research can increase costs, and APIs can become expensive when citation tokens or reasoning tokens are billed separately. Teams should treat AI search optimisation as a continuous evidence loop rather than a one-off content sprint.

Where Perplexity AI is a priority channel, the more specific playbook is to rank in Perplexity AI by making source authority, citations and topical clarity easier for retrieval systems to recognise.

| Workflow Step | What To Capture | Tooling Needed | Bottleneck | Output |

| 1. Query Classification | Informational, comparative, transactional, navigational and support prompts | Keyword data, sales questions, support logs and topic maps | Short keywords miss how users actually prompt AI systems | Controlled prompt suite |

| 2. Multi-Platform Run | Google, ChatGPT Search, Perplexity AI, Gemini and Bing Copilot answers | Logged spreadsheet, screenshots, timestamps and account notes | Answers vary by model, location, login state and freshness | Answer visibility baseline |

| 3. Citation Audit | Cited URLs, missing citations, competitor mentions and factual errors | Manual review, source logs and URL classification | Some platforms cite sources inconsistently or below the answer fold | Citation-quality score |

| 4. Content Correction | Dates, author credentials, original data, tables, FAQs and limitations | CMS edits, schema markup, editorial review and legal sign-off if needed | Thin AI rewrites can reduce trust rather than improve it | Improved source page |

| 5. Retest And Report | Citation change, answer accuracy, traffic effect and assisted conversions | Scheduled reruns and dashboard reporting | Indexing and model updates may delay measurable changes | Monthly AI search report |

As platform scale grows, teams should also monitor Perplexity AI user growth because answer-engine adoption can change faster than traditional search market share.

Takeaways

- Separate adoption metrics by behaviour: awareness, chatbot use, search-start behaviour, daily use and verified commercial impact are not interchangeable.

- Treat the 82% to 54% Fractl helpfulness drop as a warning that user confidence can fall while usage rises.

- Keep traditional SEO in the dashboard because Google still dominates global search share and AI answers are often embedded inside classic search journeys.

- Measure citation quality, not just AI answer presence, because an inaccurate or invisible citation can create risk without referral value.

- Build a weekly prompt suite across Google AI Overviews, ChatGPT Search, Perplexity AI, Gemini and Bing Copilot to reduce anecdotal reporting.

- Model subscription and API costs before scaling, especially where request fees, token fees, reasoning fees or compute-based limits apply.

- Prioritise original data, named experts, current dates and source-rich tables because answer systems compress pages that already have clear evidence structure.

- Use AI search as a parallel visibility channel, not a replacement for search, PR, content strategy or conversion analytics.

Our Editorial Verification Process

This article was built through an editorial verification process rather than a single survey scrape. The evaluation cross-referenced primary survey pages from Orbit Media and QuestionPro, Fractl, Pew Research Center, Stanford HAI, SISTRIX, Ahrefs, WordPress VIP, Google, OpenAI, Perplexity AI and platform pricing documentation available on 25 June 2026. During our 2026 evaluation, each adoption, trust, click-through and pricing claim was assigned to a source type: primary research, official vendor documentation, industry analysis, academic preprint or news reporting. Figures that measured different behaviours were deliberately kept separate, which is why adoption markers are described as signals rather than pooled into one synthetic forecast. Pricing tables only state amounts verified from official vendor pages or support documentation. Where the accessible Microsoft Copilot pricing page did not expose a stable regional public price, the article states that limitation rather than inserting an assumed figure.

Conclusion

The 2026 AI search market is not a simple story of replacement. It is a story of compression, bundling and trust. AI answers are now visible enough to shape discovery, and surveys show rapid growth in user experimentation. Yet the same evidence shows that confidence is fragile. Fractl’s helpfulness decline, WordPress VIP’s trust findings and publisher click-through studies all point to the same conclusion: adoption alone does not guarantee authority.

The next phase will be decided by attribution quality. Search platforms will need to show sources more clearly, publishers will need to structure evidence for both humans and machines, and marketers will need to measure whether AI visibility leads to trust, visits and revenue. Traditional search will remain central, but it will increasingly operate with an AI layer above, beside and inside it.

Open questions remain. Survey methods are not yet standardised. AI Overview behaviour changes quickly. Paid-plan access can alter what users see. Regional rules may reshape source display. The safest strategic posture is therefore disciplined flexibility: keep measuring classic search, build AI answer audits, protect original reporting, and treat trust as the core performance metric of AI search.

FAQs

What Is an AI Search Engine Adoption Survey?

An AI search engine adoption survey measures whether people use AI-powered tools or AI answer features to find information. Strong surveys clarify the sample, country, field date, definition of AI search, frequency of use and whether the behaviour replaces or complements traditional search.

What Does the AI Search Engine Adoption Survey 2026 Evidence Show?

It shows fast adoption but uneven trust. Pew reported US chatbot use rising to 49% in 2026, Stanford HAI estimated 53% generative AI adoption, and Fractl found 70% of consumers increased AI search use while helpfulness fell to 54%.

Is AI Search Replacing Google in 2026?

No, not fully. AI search is being used alongside traditional search, and Google still holds dominant search share. The bigger shift is that AI answers are appearing inside Google Search, ChatGPT, Perplexity AI, Gemini and Microsoft Copilot workflows.

Why Is Trust in AI Search Falling?

Trust appears to be falling because users encounter weak citations, hallucinations, generic summaries, brand misrepresentation and uncertainty about source attribution. The novelty effect is fading, so users are judging AI answers more like editorial products than demos.

Which Age Groups Use AI Search the Most?

Younger users generally adopt AI tools more heavily, but trust is more complicated. Fractl found Baby Boomers were more likely than Gen Z to rate AI search as helpful, while Gen Z was more likely to penalise brands for heavy AI use.

How Does AI Search Affect Publisher Traffic?

AI search can answer above the click, reducing visits to original pages. SISTRIX found German organic click rates fell when AI Overviews appeared, while Ahrefs reported lower average click-through rates for top-ranking pages on AI Overview queries.

What Should Marketers Track for AI Search?

Marketers should track classic rankings, AI answer inclusion, cited URLs, citation accuracy, brand sentiment, competitor mentions, click-throughs, assisted conversions and factual errors. Screenshots alone are not enough because AI answers vary by query and model.

Are AI Search Pricing Plans Comparable?

Only partly. ChatGPT, Gemini, Perplexity AI and Copilot package search through different subscription, workspace and API models. Usage caps, compute limits, request charges, token fees and regional eligibility can matter more than headline monthly prices.

References

- Xu, H., Iqbal, U., & Montgomery, J. M. (2026). Measuring Google AI Overviews. arXiv. https://arxiv.org/abs/2605.10985

- WordPress VIP. (2026). Brands race to be seen by AI, but consumers still demand trust and attribution. https://wpvip.com/resource/brands-race-ai-content-discoverability/

- SISTRIX. (2026). AI Overviews in Germany: Click impact analysis. https://www.sistrix.com/blog/ai-overviews-in-germany-click-impact/

- Pew Research Center. (2026). Americans and AI in 2026. https://www.pewresearch.org/internet/2026/05/21/americans-and-artificial-intelligence-in-2026/

- Perplexity AI. (2026). Enterprise pricing and Sonar API documentation. https://www.perplexity.ai/enterprise and https://docs.perplexity.ai/

- Maslej, N., Sajadieh, H., Perrault, R., Parli, V., Reuel, A., Brynjolfsson, E., Etchemendy, J., Ligett, K., Lyons, T., Manyika, J., Ngo, H., Niebles, J. C., Shoham, Y., Wald, R., & Clark, J. (2026). The AI Index 2026 annual report. Stanford Institute for Human-Centered Artificial Intelligence. https://aiindex.stanford.edu/report/

- Google. (2026). A new era for AI Search. https://blog.google/products/search/google-search-ai-mode-ai-overviews-io-2026/

- Fractl. (2026). AI Search Consumer Trust Study. https://www.fractl.com/blog/ai-search-consumer-trust-study/

- Crestodina, A. (2026). The AI-Search Adoption Survey. Orbit Media Studios. https://www.orbitmedia.com/blog/ai-search-adoption-survey/