At $26.13 a share, SoFi Technologies has become one of the most closely watched fintech stocks in early 2026. The price reflects far more than a single trading session’s -1.17 percent dip. It captures a year of dramatic transformation, exuberant gains, and a sobering reminder of how quickly sentiment can turn when growth collides with dilution.

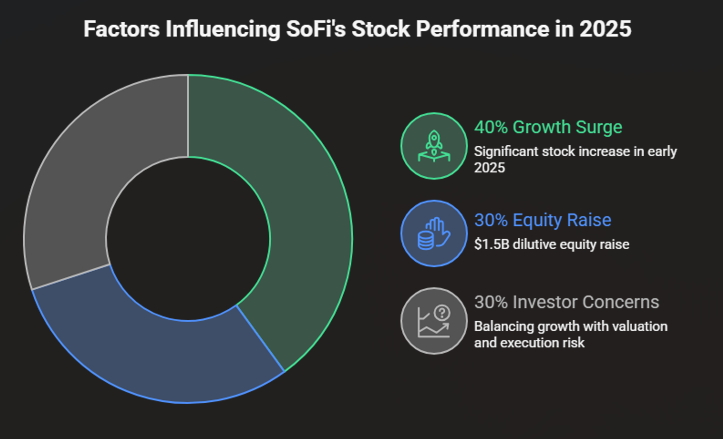

For investors searching for clarity, the central question is straightforward: is SoFi still a high-growth financial disruptor temporarily bruised by capital raising, or has its stock run too far, too fast? In the first hundred words of any serious discussion of SoFi stock, the answer begins with scale. The company has grown from a niche student-loan platform into a diversified digital financial services firm with banking, investing, lending, and crypto exposure. That expansion helped push the stock from roughly $7.83 in January 2024 to above $30 by late 2025, a gain of more than 70 percent year over year entering 2026.

Yet success brought consequences. In December 2025, SoFi announced a $1.5 billion public stock offering, its second major equity raise of the year. The move strengthened the balance sheet but diluted existing shareholders, triggering immediate sell-offs and renewed skepticism from Wall Street analysts. With earnings, valuation, and macro pressures now intersecting, SoFi stock has become a test case for how markets price growth in an era of higher rates and tighter scrutiny.

Where SoFi Stock Trades Today

As of the latest data, SoFi stock trades at $26.13 on the NASDAQ, near the lower end of its recent range. The day’s trading fluctuated between $26.01 and $26.78, with volume around 40.3 million shares, below the three-month average of 63.4 million. The market capitalization stands at approximately $32.94 billion, reflecting the impact of newly issued shares following the December offering.

From a technical perspective, the stock sits below its 50-day moving average of $27.58 but comfortably above its 200-day average of $22.03. This positioning illustrates the tension between short-term caution and longer-term upward momentum. The year’s high of $32.73 contrasts sharply with a low of $8.60, underscoring how volatile the journey has been for shareholders.

Fundamentally, SoFi reports earnings per share of $0.56 and trades at a price-to-earnings ratio of roughly 46.66. That valuation places it firmly in growth-stock territory, leaving little room for disappointment. Investors are not paying for what SoFi is today, but for what it promises to become.

A Fintech Built on Relentless Expansion

SoFi’s story is inseparable from its aggressive expansion strategy. Over the past several years, the company has transformed into a one-stop digital financial platform, offering personal loans, student loan refinancing, mortgages, credit cards, brokerage services, and cryptocurrency trading under one app. Its acquisition of a bank charter allowed it to fund loans with deposits rather than wholesale markets, improving margins and flexibility.

Membership growth has been a cornerstone of the bull case. By the end of 2025, SoFi reported approximately 9.5 million members, a record figure that reinforced its narrative of scale and engagement. Each new product cross-sold to existing members deepens lifetime value, at least in theory.

This growth, however, requires capital. Unlike mature banks that generate surplus cash, SoFi remains in an investment-heavy phase. Technology spending, marketing, regulatory compliance, and product development all demand funding. The December 2025 stock offering must be viewed through this lens: as fuel for ambition rather than a sign of distress.

Read: AI Adoption in 2026: Which Countries Are Moving Fastest Worldwide

The $1.5 Billion Stock Offering Explained

In early December 2025, SoFi announced a $1.5 billion public offering priced at $27.50 per share. The deal issued approximately 54.5 million new primary shares, with underwriters granted a 30-day option to purchase up to 15 percent more, or about 8.2 million additional shares. If fully exercised, the total issuance could reach 62.7 million shares.

Before the offering, SoFi had roughly 1.20 to 1.26 billion shares outstanding, based on third-quarter 2025 filings. The new issuance increased that count by approximately 4.3 percent at the base level and up to about 5.2 percent if the greenshoe option was fully exercised. By early January 2026, shares outstanding were estimated at between 1.255 and 1.325 billion.

The market reacted swiftly. Shares fell 6 to 8 percent, sliding from around $29.60 toward the $27.50 offering price. Trading volume surged roughly 74 percent above average as investors recalibrated their expectations for earnings per share and ownership dilution.

Dilution in Numbers

| Metric | Pre-Offering | Post-Offering (Base) | Post-Offering (Max) |

|---|---|---|---|

| Shares Outstanding | ~1.20B | ~1.255B | ~1.325B |

| New Shares Issued | — | 54.5M | 62.7M |

| Dilution Impact | — | ~4.3% | ~5.2% |

Dilution does not automatically destroy value, but it does change the math. Earnings must now be spread across a larger share base, putting pressure on per-share metrics even if total profits grow.

Market Capitalization: A Subtle Trade-Off

Interestingly, the stock offering increased SoFi’s market capitalization by nearly the same amount as the capital raised. At $27.50 per share, the issuance generated exactly $1.5 billion in new equity. With full underwriter participation, that figure could rise to $1.725 billion.

Before the announcement, SoFi’s market cap hovered around $32 to $33 billion, based on a share price near $29 and approximately 1.20 billion shares outstanding. After the deal closed on December 8, 2025, the market absorbed the new shares, and the market cap stabilized in the $32.9 to $34.6 billion range. The current figure of $32.94 billion reflects subsequent price fluctuations rather than structural erosion.

This dynamic explains why some long-term investors view the offering as neutral. Ownership percentages shrank, but the company’s financial resources expanded without taking on debt. The question becomes whether management can deploy that capital effectively enough to justify the dilution.

Analyst Reactions: A Divided Street

Wall Street’s response to the offering was mixed, leaning cautious. On January 6, 2026, Bank of America maintained an “underperform” rating on SoFi stock, while raising its price target to $20.50. The firm cited valuation concerns and dilution risk, triggering an additional 8 to 10 percent drop as the stock slid toward $26.47.

Other firms were less bearish. Barclays reiterated a more constructive view, maintaining a price target around $28. Analysts there acknowledged dilution but emphasized member growth and long-term revenue potential.

The divergence reflects broader uncertainty about fintech valuations in 2026. With interest rates higher and investors rotating out of high-multiple growth stocks, companies like SoFi face tougher scrutiny. As one market strategist put it, “SoFi is priced like a disruptor but judged like a bank, which makes every capital decision controversial.”

Crypto Exposure and Macro Headwinds

SoFi’s diversified platform includes cryptocurrency trading, which has proven to be both an asset and a liability. In early 2026, Bitcoin’s shaky start weighed on sentiment, and SoFi began trading as a kind of “crypto proxy” in the eyes of some investors. When digital assets fall, SoFi stock often feels the ripple effect.

At the same time, rising concerns about credit losses have emerged. As a lender, SoFi is exposed to consumer credit cycles. Higher interest rates and economic uncertainty raise questions about default risk, even as loan volumes grow. These pressures compound the valuation challenge posed by a P/E ratio north of 45.

Sector rotation has not helped. Investors have shown renewed interest in value and dividend-paying stocks, leaving growth-oriented fintech names more vulnerable to pullbacks.

Expert Perspectives on SoFi’s Crossroads

A fintech analyst at a major research firm noted, “SoFi’s dilution is not excessive by growth-company standards, but its valuation amplifies every misstep.” Another observer emphasized execution risk: “Raising capital is easy. Turning that capital into durable earnings growth is the hard part.”

A banking industry consultant offered a longer view. “SoFi is building something closer to a digital universal bank. The market is impatient, but these models take time to mature.”

Together, these perspectives underscore that SoFi’s challenge is not survival, but credibility. Investors need proof that scale will translate into sustainable profitability.

Performance in Context

| Metric | Value |

|---|---|

| Share Price | $26.13 |

| Daily Change | -1.17% |

| Market Cap | $32.94B |

| EPS | $0.56 |

| P/E Ratio | 46.66 |

| 52-Week High | $32.73 |

| 52-Week Low | $8.60 |

These numbers tell a story of ambition tempered by realism. SoFi is no longer a speculative penny stock, but neither is it a settled blue chip.

Takeaways

- SoFi stock trades around $26 after a significant December 2025 offering

- The $1.5 billion raise diluted shares by roughly 4 to 6 percent

- Market capitalization remained relatively stable despite price pressure

- Analysts are split, with valuation concerns dominating bearish views

- Crypto exposure and credit risk add volatility to the outlook

- Strong member growth underpins the long-term bull case

- Execution will determine whether dilution proves worthwhile

Conclusion

SoFi Technologies stands at a defining moment. Its stock price reflects both extraordinary growth since early 2024 and the sobering realities of scale. The $1.5 billion share offering was not a sign of weakness, but it was a reminder that growth has a cost. For shareholders, that cost arrived in the form of dilution and heightened scrutiny.

The coming quarters will be decisive. If SoFi converts its expanded balance sheet into accelerating earnings and disciplined risk management, today’s valuation may appear justified in hindsight. If not, the stock’s premium multiple leaves little margin for error.

In the broader context, SoFi’s journey mirrors that of the fintech sector itself: bold, fast-moving, and increasingly accountable. The market is no longer rewarding growth alone. It is demanding proof. For SoFi investors, patience and realism may matter as much as optimism.

FAQs

Why did SoFi issue new shares in 2025?

To raise $1.5 billion in equity to fund growth initiatives, acquisitions, and balance-sheet strength.

How much dilution did the offering cause?

Approximately 4.3 percent at the base level and up to about 5.2 percent if underwriters exercised their option.

Is SoFi still a growth stock?

Yes, but its high P/E ratio means growth must translate into earnings to sustain valuation.

How does crypto affect SoFi stock?

Crypto exposure adds volatility, especially when digital asset prices decline.

What do analysts think about SoFi now?

Opinions are mixed, ranging from underperform ratings to cautious optimism around long-term growth.